2013年10月4日米国カリフォルニア州キャンベル発―Infonetics Researchはスモールセル機器の市場規模と予測レポートからの抜粋を公表した。レポートでは、3Gマイクロセル、ピコセル、メトロセルおよび4G LTE mini eNodeBとメトロセルについて追跡調査している。

アナリストノート

Infonetics Researchでモバイルインフラと通信事業者エコノミックスを担当する主席アナリストStephane Teral氏は次のように説明する。「大手サービスプロバイダーはスモールセル展開プランへの取り組みを維持していますが、そのペースは悲しい現実によって予想よりはるかにゆっくりしたものになっています。スモールセルとマクロセルの投入には何も共通するものがないのです。」

Teral氏はこう続ける。「スモールセルとマクロセルはそれぞれ技術的に独自の内部業務プロセスを必要とします。マクロセルには数十年間の下地がありますが、スモールセルは足回り、回帰経路の可用性、建物の寸法、ワイヤレス技術などを考慮に入れてゼロから構築しなければなりません。スモールセルの展開には、これといった決まった方式がないのです!」

レポートの共著者であり、Infoneticsでマイクロ波と通信事業者WiFiを担当するアナリストRichard Webb氏はこう付け加える。「サービスプロバイダがこれからの攻め方を練り直している最中だと考えると、スモールセルの盛り上がりが2013年に起こることはないと予想しています。」

スモールセル市場のハイライト

- 通信事業者がスモールセルを展開する主な目的は、収容力の観点からマクロセル レイヤーを補完増強し、モバイル ブロードバンド体験を改善することである。

- 2014年の早い段階で、ショッピングモールやスタジアム、交通機関の停留所、ホテル、イベント会場などでの屋内展開の必要性から4Gメトロセルがスモールセル市場成長の主力要因になるだろう。

- アジア太平洋地域は、10万ヶ所以上の設置箇所を持つ最大密度のマクロセル ネットワークが、中国、日本、韓国に見られるように、動きの激しい地域であり、2017年を過ぎてもそのままであり続けるだろう。

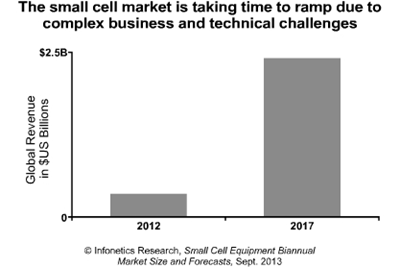

- Infoneticsは世界のスモールセル市場が2017年までに24億ドル規模に成長すると見込んでいる。

Infonetics' biannual small cell report provides worldwide and regional market size, forecasts through 2017, analysis, and trends for 3G microcells, picocells, and metrocells and 4G (LTE) mini eNodeB and metrocells. The report also includes a small cell strategies tracker. Vendors tracked: Airspan, Airvana, Alcatel-Lucent, Alvarion, Argela, BelAir, Contela, Ericsson, Huawei, ip.access, Juni, Minieum, NEC, NSN, Samsung, SK Telesys, SpiderCloud, Ubiquisys, ZTE, and others.

(原文)

Small cell ramp won't happen this year

Campbell, CALIFORNIA, October 4, 2013-Telecom market research firm Infonetics Research released excerpts from its latest Small Cell Equipment market size and forecast report, which tracks 3G microcells, picocells, and metrocells and 4G LTE mini eNodeBs and metrocells.

ANALYST NOTE

"The large service providers remain committed to their small cell deployment plans, but the pace of deployment is much slower than expected due to a sad reality: Small cell and macrocell rollouts share nothing in common," explains Stephane Teral, principal analyst for mobile infrastructure and carrier economics at Infonetics Research.

Teral continues: "Each technology requires its own internal business processes, which have been in place for decades with macrocells but have to be built from the ground up for small cells taking into consideration things like footfall, building dimensions, backhaul availability, and wireless technology. There is no cookie-cutter template for small cell deployments!"

Co-author of the report Richard Webb, directing analyst for microwave and carrier WiFi at Infonetics, adds: "Given that service providers are in the process of retooling their plan of attack, we're not expecting the small cell ramp to happen in 2013."

SMALL CELL MARKET HIGHLIGHTS

- Operators' chief purpose for deploying small cells is to complement and enhance the macrocell layer from a capacity standpoint, to enrich the mobile broadband experience

- Beginning in 2014, 4G metrocells will become the main growth engine in the small cell market, driven by in-building deployments in retail malls, stadiums, transportation stations, hotels, and event venues

- Asia Pacific is where the action is and where it will stay through 2017: The largest macrocell network density, with more than 100,000-site footprints, can be found in China, Japan, and South Korea

- Infonetics forecasts the global small cell market to grow to $2.4 billion by 2017