アナリストノート

Infonetics Researchの共同設立者兼通信事業者ネットワークの主席アナリストであるMichael Howard氏は次のように説明する。「2013年は屋外用スモールセル導入が大きく進む年になるはずでしたが、導入は事業者の期待通りの早さで進んでいません。事業者にとっては、ちょっと外にピクニックに行ってくるというような簡単な作業ではないのです。費用は予想よりも大きくかさみ、解決の難しい課題が山積みです。例えば、立地、管轄の問題、地域における未決着の規制、電力の可用性、銅線や光ファイバーの可用性、スモールセルにバックホールを同梱するかどうかの問題、利用できるようになったばかりの技術や製品をどうするか、バックホールとの接続をどうするかなど、たくさんの課題があります。LTEや将来的にはLTEアドバンストとの厳密な時間調整や同期、レイテンシーの要件をサポートする必要のある新しいタイプのバックホール上で、WiFiや近傍のマクロセルとスモールセルをどのように調整するかについては言うまでもありません。」

アナリストノート

Infonetics Researchの共同設立者兼通信事業者ネットワークの主席アナリストであるMichael Howard氏は次のように説明する。「2013年は屋外用スモールセル導入が大きく進む年になるはずでしたが、導入は事業者の期待通りの早さで進んでいません。事業者にとっては、ちょっと外にピクニックに行ってくるというような簡単な作業ではないのです。費用は予想よりも大きくかさみ、解決の難しい課題が山積みです。例えば、立地、管轄の問題、地域における未決着の規制、電力の可用性、銅線や光ファイバーの可用性、スモールセルにバックホールを同梱するかどうかの問題、利用できるようになったばかりの技術や製品をどうするか、バックホールとの接続をどうするかなど、たくさんの課題があります。LTEや将来的にはLTEアドバンストとの厳密な時間調整や同期、レイテンシーの要件をサポートする必要のある新しいタイプのバックホール上で、WiFiや近傍のマクロセルとスモールセルをどのように調整するかについては言うまでもありません。」Infoneticsでモバイル バックホールとスモールセルを担当するアナリスト、Richard Webb氏はこうつけ加える。「これは当社の最新の予測と合致しています。当社は2013年から2017年の5年間にわたって事業者が屋外用スモールセル バックホール機器に使う費用は、事業者の計画に基づいた以前の予測よりも低い36億ドルになると見積もっています。」 スモールセルおよびLTEバックホール調査のハイライト

- 事業者は屋外用スモールセル導入の費用が予測より高いことに気付きつつある: より多くの回答者が、通常のマクロセル導入に対してスモールセル導入にかかる5年間のTCO(Telecom Operator)の割合が、Infoneticsによる2012年の調査時の10%よりも高い25%になると今では予測している。

- 密集都市部においてはポイント?ツー?マルチポイント (P2MP) バックホール接続形態に大きなチャンスがあるが、今日P2MP製品を出荷するメーカーはほんの数社しかない: BluWan、Cambridge Broadband、Intracom。

- 調査対象の事業者のうち4分の1は、2016年以降までに屋外用スモールセル バックホール ネットワークにソフトウェア定義ネットワーク (SDN) を利用すると表明した。

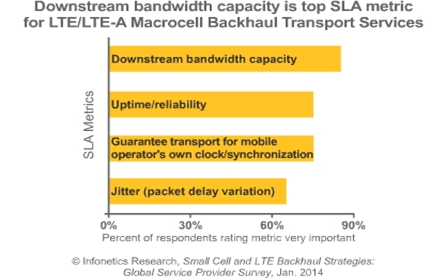

- ダウンストリームの帯域幅容量は、LTEおよびLTEアドバンスト (LTE-A) をサポートするバックホール サービスにおけるサービスレベル契約 (SLA) の最重要基準である。

Outdoor small cell challenges mount, stymieing deployments Campbell, CALIFORNIA, February 21, 2014-Market research firm Infonetics Research released excerpts from its Small Cell and LTE Backhaul Strategies: Global Service Provider Survey, which provides insights into operator plans for small cell and macrocell backhaul. ANALYST NOTE "2013 was supposed to be the year for greater deployments of outdoor small cells, but installations haven't proceeded as quickly as operators expected. It's no picnic out there for operators. Costs are higher than anticipated, and many challenges remain difficult to solve, including siting, jurisdictional issues, unsettled local regulations, power availability, copper and fiber availability, small cell packaging with or without backhaul, just-coming-available technologies and products, and backhaul connections. Not to mention the coordination of small cells with WiFi or nearby macrocells over new types of backhaul that must support strict timing, sync, and latency requirements for LTE and LTE-Advanced in the future," explains Michael Howard, co-founder and principal analyst for carrier networks at Infonetics Research.

Richard Webb, Infonetics' directing analyst for mobile backhaul and small cells, adds: "This is in line with our recent forecast in which we project that operators will spend $3.6 billion on outdoor small cell backhaul equipment over the five years from 2013 to 2017, down from earlier forecasts based on operator plans." SMALL CELL AND LTE BACKHAUL SURVEY HIGHLIGHTS

- Operators are finding that outdoor small cell deployments are more expensive than anticipated: more respondents now expect the 5-year TCO ratio of a small cell deployment to be 25% of a typical macrocell deployment, up from 10% in Infonetics' 2012 survey

- There is a big opportunity for point-to-multipoint (P2MP) backhaul topology in dense urban areas, but there are only a few manufacturers shipping P2MP products today: BluWan, Cambridge Broadband, and Intracom

- 1/4 of operators surveyed indicated they will use software-defined networking (SDN) in outdoor small cell backhaul networks by 2016 or later

- Downstream bandwidth capacity is a top service-level agreement (SLA) metric for backhaul services supporting LTE and LTE-Advanced (LTE-A)